Dear West Shore Village owners and residents:

Our recent plan to secure a line of credit to help us with the property insurance premiums has provided a fertile environment on Facebook for uninformed personal opinions. As everyone is seeking more details on this plan, it is imperative that the information provided is sufficient and based on facts. Hopefully, the following points will help to clarify many questions raised by our residents.

For additional information please refer to the 2023 – 2024 Budget Overview posted at the West Shore Village Website or email us at wsvbb1@gmail.com.

How were the insurance premiums budgeted in the past?

Until and including the Fiscal Year 2017/18 the insurance budget was part of the Master Reserves. This made it easier for the previous boards to budget and pay for the insurance premiums and there was no need to ask the owners for permission to use reserves to pay for insurance. Any shortfall in reserve funds due to higher insurance premiums was made up by assessments for other reserve items. However, having the insurance budget as part of reserve funds is the equivalent of including in reserves such recuring expenses as payroll or electricity. Therefore, to correct this issue, starting with the Fiscal Year 2018/19, the insurance became part of the operations budget.

Borrowing funds from reserves for insurance

We are allocating a portion of our operating budget to a separate Insurance Fund. The amount of the monthly allocations is calculated every year to ensure availability of sufficient funds to pay property and flood insurance premiums in November and December, without using reserves. Due to reasonably accurate estimates of the insurance premiums increases, we were able to accomplish that every year until November 2022.

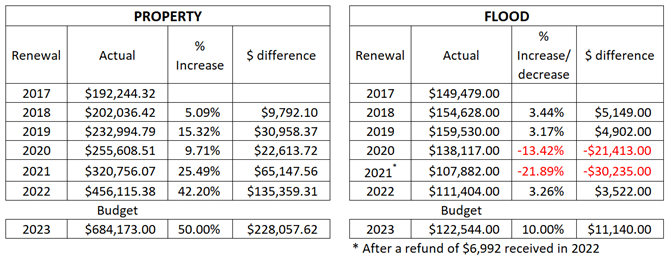

2022/23 Property Insurance Renewal

Our 2022/23 Budget included an estimated 20% increase in property insurance premiums due November 1, 2022. With a 20% increase the Association would have been able to pay the entire amount from the Insurance Fund on the due date. However, as we are painfully aware, the actual increase was 42%. Disappointingly, we had no choice but to borrow funds from reserves. These funds were returned to reserves in April 2023.

2023/24 Insurance Budget

To reflect the disastrous insurance environment in Florida, our 2023/24 Budget includes a 50% increase in property premiums. This was done against objections of some owners who questioned why we need to budget for such a high increase.

With this increase, we could no longer afford to budget monthly allocations that would provide us with sufficient funds in November and December 2023. Thus, these contributions had to be prorated to an entire fiscal year. We will need to borrow funds from reserves when the renewals are due in November and December.

The property insurance increases are now 50% to 100%, and even 150%. If the increase is above 50%, we are not going to have enough funds in our reserves. Hence the need for the line of credit. Based on the bank’s terms for this type of credit line, we can use it only to pay for insurance premiums. The maximum repayment period is 11 months.

Additional insurance renewal consideration

While we are facing a substantial increase in insurance premiums, there is also a risk that our carrier may not renew our property insurance contract at all. That is why we are proactively preparing for a possibility of having to get our insurance from Citizens. This will need some preliminary steps (and expenses) on our part. Citizens will need Wind Mitigation Inspection reports for all our buildings. This will cost $7,370 for the remaining 67 buildings which don’t have current reports. In addition, we will also need electrical inspections for 20 buildings. We are waiting for quotes from electrical contractors.

Aligning the insurance period with our Fiscal Year

There is very little room for making such an adjustment.

- According to the Association docs, our Fiscal Year starts on April 1st.

- After the latest Bylaw amendment, the budget is approved at the Annual Meeting in early March.

- The Annual Meeting is preceded by a 30-day mailing to owners, i.e., early in February.

- Therefore, to compile this mailing, the budget must be completed before the end of January.

- The insurance carriers can only quote 30 days before the renewal date.

- The Budget Committee and the Board must allow adequate time for meetings and discussions with the insurance agent before reaching an agreement on final adjustments of the property insurance renewal.

Considering that date of the Annual Meeting was changed from February to March, the property insurance due date could be changed from November 1st to December 1st. The Board will need to decide if a change of one month is worth the effort.

Audit

Audits of the West Shore Village Master Corporation were performed in 2012, 2015 and 2020. The last audit of the financial statements of WSV was carried out by Bashor and Legendre, LLP and completed in July 2020. The results of this audit can be found on OneSource, folders: Property Information/Year End Financial Reports. The accounting firm charged $6,000.00 to perform the audit.

Fees increased from $450 in 2021 to $825 in 2023

The 2023/2024 budget was affected by several significant increases, such as property insurance, roofs, water consumption and electricity. While these increases affected all villages, owners of units in Village 3 have been affected the most due to three roofs to be replaced in the next 2 years and the 27% increase in cost of roof replacements. As a result, Village 3 reserve contributions went up significantly in 2023/2024 budget and the monthly fees of 2-bedroom units (1,179 square feet) in Village 3 raised to $829.04. The same units were paying $558.06 in 2021/2022 and $473.45 in 2018/2019.

Self insuring

The following is an excerpt from Campbell Property Management Webinar on April 25, 2023.

“And regards to self insurance. It comes up a lot right now because we’re seeing such steep rate increases. Unfortunately, it’s not practical, because you have high concentration of values in a very small, concentrated area and banks are not going to look at all favorably on that. So, in a unit owner’s case that have bank loans, self insurance is not going to be accepted and if there is a loss, the directors could be liable for making a bad decision. Also, condo law requires that associations carry insurance, so all those things really prohibit self insurance from being practical.”

Full recording of the April 25/23 webinar can be accessed at this link.

WSV Amenities (There is $80K set aside for new tennis/pickle ball courts.)

One of the fiduciary duties of the Board is to maintain the existing amenities of the Association. This includes the swimming pool, the clubhouse, and the tennis and shuffleboard courts. Many of our current owners purchased their units to enjoy these recreational facilities and they must be kept up to maintain property values and attract new buyers. The funds for periodic refurbishments or replacements of these amenities are included in the WSV Master Reserves. Thus, as the Clubhouse may need a new roof every 25 to 30 years, the swimming pool geothermal heaters need periodic repairs and the tennis courts need to be replaced when the surface is becoming a safety issue to residents using the courts.

Insuring all buildings for flood

According to our attorney’s statement in October 2021, we must carry flood coverage for the entire association. Ignoring a legal advice would make the Board liable for a bad decision. As there have been a number of legislative changes during the past 6 months as well as updates of FEMA processes, this issue will be reviewed again prior to the next renewal.

WSV Staff (employees and payroll. Unused funds from resignations. Replacing vacancies)

The WSV Board proposes and approves hourly rates of the WSV maintenance and landscaping employees, and that is exactly what they are paid. If an employee resigns, the “saved” salary is left in our operations account. These savings can be used for other line items, or in the current case of two resignations, for hiring a temporary landscaping contractor. There are other unexpected expenses, such as the Wind Mitigation Inspections, and savings from one line item is applied to another as needed. None of that money is “kept” by RPM.

RPM and the Board are urgently trying to replace the landscaping staff. Unfortunately, there are more vacancies than candidates at this time and it may take a few months to find suitable employees.

RPM (We pay RPM more than $240K)

The annual Management Fee is $42,660 for 2023/24 Fiscal Year.

Salaries, tax burden and insurance checks for WSV staff are processed by RPM on behalf of the WSV Association.

Financial planning, freezing non-essential spending.

The operations budget doesn’t include any discretionary spending. Any cuts would adversely affect the Board’s ability to maintain the WSV property.

Current insurance due (why isn’t RPM working on it to get ahead of the game?)

The property and flood insurance due dates are November 1st and December 20th respectively.

The Board, RPM and our insurance are proactive in preparing for the renewals. We are getting Wind Mitigation Inspections done on 67 buildings, electrical inspections done on 20 buildings built before 1975 and we are replacing 7 roofs.

Assessment – what would the numbers be?

A 100% increase in property insurance premiums would result in an assessment of approximately $1,500 for a two-bedroom unit.

Getting a letter with new fees only 3 weeks before

The new fees are included in a “30 day” mailing to owners, i.e., 1 month prior to the annual meeting, which is held approximately 3 weeks before the end of our fiscal year. Thus, the owners are informed of the new fees 6 to 7 weeks before the new fees are due.

Insufficient reserves, obvious shortfalls.

Reserve funding is required for community associations under Florida Statute 718.112. The components included in WSV reserve accounts, their estimated remaining useful life and estimated replacement costs are based on a Reserve Study performed by FPAT in 2019 for 2019/2020 budget. The replacement costs are updated annually for components that are being replaced periodically, such as roofs, painting, sidewalk replacements or tenting for termites. Replacement costs of some other, non-frequent items have not been updated since the reserve study.

A reserve study should be done every three to five years and we are due for a new one. Considering the recent price increases of projects and services, WSV Association should get a new Reserve Study done prior to 2024/25 Budget.

Past Property and Flood Insurance Premiums and the current Budget